How reciprocal relationships appear one-sided when contributions become invisible #

Ledger/Visibility Collapse is when selective accounting makes reciprocal relationships appear one-sided by making some contributions visible while others become structurally invisible.

This is not about one party being ungrateful or exploitative (though it can become that). This is about which items appear on the ledger and which items disappear into baseline.

It shows up in geopolitics, client relationships, personal relationships, and institutional partnerships. Once you see it, you see it everywhere.

Why it feels like ingratitude #

When you are on the giving side of an invisible contribution, it feels like:

- They don’t appreciate what I do

- They think they’re entitled to my help

- They’ve forgotten everything I’ve done for them

- Gratitude never comes

That feeling is real. But the problem is not virtue. The problem is visibility.

The ledger is structurally incomplete, so they literally cannot see what they should be grateful for. The contribution has become baseline. Baseline feels like entitlement because it is experienced as continuity, not as gift.

You cannot be grateful for what you cannot see.

That is the trap. And it is not personal. It is structural.

The pattern in action #

Example 1: US-Europe defense relationship #

Visible ledger items (what gets counted):

- US defense spending as percent of GDP

- Direct military aid

- Equipment transfers

- Troop presence costs

Invisible ledger items (what becomes baseline):

- Basing rights and host-nation infrastructure

- Logistics throughput (Ramstein, Rota, Landstuhl)

- Air corridors and operational access

- Intelligence sharing and interoperability

- Coalition legitimacy and political cover

- Market access and regulatory cooperation

The US political conversation collapses to: “We spend, they don’t.”

The full exchange includes: “We spend, and we get operational geometry that enables global power projection, rapid response, and strategic deterrence.”

Both are true. Only one is visible in the accounting.

Most of the US security establishment understands this perfectly well. Ramstein and Landstuhl are not charity, they are core nodes in US global posture. Naval Station Rota in Spain is a major US Navy hub. These are not gifts to Europe. These are strategic assets that enable US power projection into Africa, the Middle East, and beyond.

But that full ledger does not fit into domestic political rhetoric. So the conversation collapses to one visible line item: spending. Everything else becomes invisible background.

Example 2: Anonymous client relationship #

Visible ledger items:

- Percentage of sales or billable hours

- Contracted deliverables

- Scheduled meetings

Invisible ledger items:

- “Growth work” done to protect outcomes

- Strategy consultation beyond maintenance scope

- Network connections and introductions

- Problem-solving that prevents future crises

- Infrastructure built on speculation with no upfront payment

The client’s ledger shows: “We pay for services, we get services.”

Your ledger shows: “I built this on speculation, absorbed all the startup risk, deliver contracted work plus significant extras that I do because I’m incentivized by outcomes, and now they begrudge me when we have a good month.”

Over time, the extras become expected. When you try to return to baseline scope, you look like you withdrew support. They don’t see themselves as having lost a gift. They see you as having broken the deal.

This is especially acute in outcome-based compensation where you cannot easily withdraw extras without threatening your own revenue. The client learns to expect everything you do to protect outcomes, even when it is far beyond original scope.

Example 3: Personal relationships #

Visible ledger items:

- Direct requests fulfilled

- Explicit favors

- Financial support

Invisible ledger items:

- Emotional labor and active listening

- Schedule flexibility and accommodation

- Network effects and social capital

- Conflict absorption and peace-keeping

One person feels: “I do everything and get nothing back.”

The other person feels: “What are you talking about? We split everything.”

Both ledgers are incomplete. Neither is lying. The relationship has Ledger/Visibility Collapse.

The baseline drift mechanism #

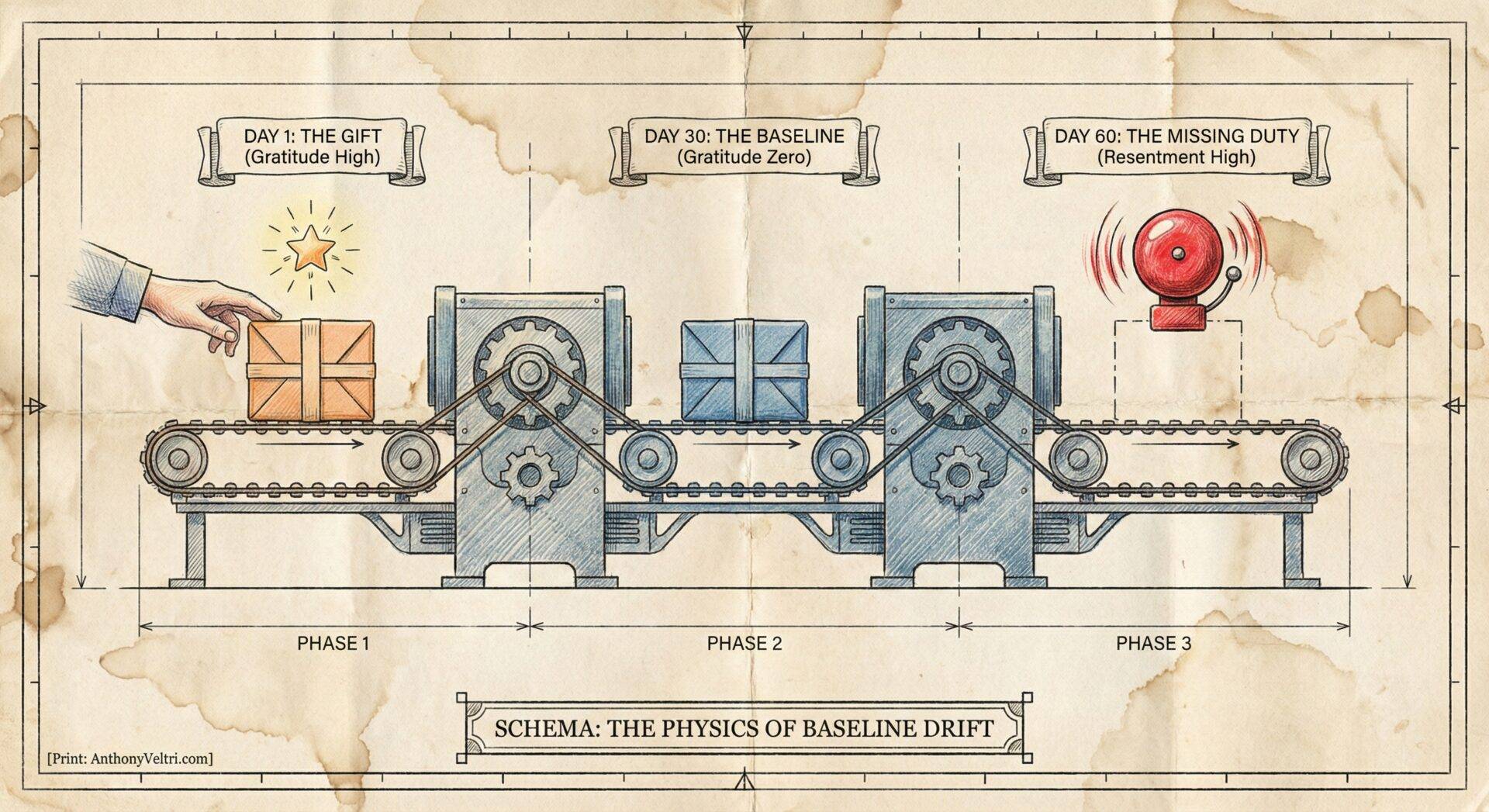

Definition: Baseline Drift is the phenomenon where an extraordinary effort, repeated twice, becomes a standard expectation. The speed at which a gift degrades into a duty.

Ledger/Visibility Collapse is not random. It follows a predictable three-stage process:

Stage 1: Baseline drift #

Once an “extra” exists for more than one cycle, it becomes the new normal.

People plan budgets, staffing, and expectations around it. It stops being perceived as gift and starts being perceived as structure.

This is not malice. This is how human planning works. Reliable inputs become assumed inputs. If you deliver something twice, it becomes expected. If you deliver it three times, it becomes required.

Stage 2: Entitlement via dependence #

Dependence feels like ownership.

When something becomes load-bearing in your operations, you experience its removal as a threat, not as the withdrawal of a gift.

“We need it” becomes “you should provide it” becomes “you owe it to us.”

This progression is structural, not moral. The person is not necessarily being entitled in the traditional sense. They are responding rationally to dependence. If you have built your operations around an input, that input feels like infrastructure, not charity.

Stage 3: Salience asymmetry #

What the receiver experiences: Continuity. The benefit flows without friction, so it becomes invisible.

What the giver experiences: Cost. Every delivery requires effort, so it remains visible.the

The receiver sees: “Everything is working.”

The giver sees: “I am carrying this.”

This is the visibility collapse. The contribution becomes invisible to the receiver precisely because it is reliable. The more dependable you are, the more invisible you become.

That is the structural trap. Competence creates invisibility.

Why this is structurally dangerous #

Ledger/Visibility Collapse does not just create resentment in one relationship. It creates perverse incentives across the system.

If invisible contributions don’t get counted, people learn:

- Don’t invest in maintenance. It becomes invisible.

- Don’t build durable infrastructure. It becomes baseline.

- Don’t enable others’ success. It becomes expected.

- Do deliver visible, episodic wins. They stay countable.

This is why systems degrade. Not because people are lazy, but because the incentive structure rewards visible intervention over invisible stewardship.

The reliable infrastructure that prevents crises never gets credit. The firefighter who shows up after the crisis does.

This is the same dynamic that makes preventive maintenance impossible to fund. You cannot prove you prevented something. You can only prove you fixed something after it broke. So the incentive structure rewards letting things break.

The outcome-based compensation trap #

There is a specific structural condition that accelerates Ledger/Visibility Collapse: when you are paid on outcomes rather than inputs, you absorb scope creep to protect your revenue, but the client never sees the cost.

#

In both cases—my family’s single restaurant and the modern MSP—the mechanism is the same: competence creates invisibility.

The Family Parable: The One-Restaurant Trap This is not a hypothetical. My family lived this. When I was a kid, our family ran a construction company that (among other things) built a single large restaurant. Because the deal was structured on a percentage of the restaurant’s future success, we didn’t just build a building; we married a risk.

We stopped being builders and became accidental operators.

We found ourselves training chefs. We found ourselves covering weekend shifts. We found ourselves managing inventory. We did none of this because we wanted to be restaurateurs; we did it because we needed that specific restaurant to survive so we could get paid for the building.

The owner never saw a bill for chef training. They just saw “support.” It became baseline. When we tried to stop, they didn’t say, “Thanks for the extra help.” They said, “Why are you abandoning me?”

The Modern Version: The Managed Services Trap If the construction story feels specific, the digital version is universal.

Consider the Managed Service Provider (MSP) paid a flat monthly fee to “keep the servers up.” To keep the uptime high, the MSP starts quietly fixing the client’s terrible code.

- Visible Ledger: “Server Uptime: 99.9%.”

- Invisible Ledger: The MSP rewriting bad SQL queries at 3 AM so the database doesn’t crash.

The client thinks their code is fine. The MSP knows the code is trash. When the MSP finally stops doing the invisible shadow-coding, the site crashes. The client blames the MSP.

That is Ledger/Visibility Collapse accelerated by outcome-based compensation.

The mechanism #

Outcome-based compensation creates three structural problems:

- Scope creep without visibility

- You do extra work to protect your outcomes

- The client never sees the cost because it is not itemized

- The extra work becomes invisible by design

- The success penalty

- The better you protect outcomes, the more extras you absorb

- The more extras you absorb, the more the client expects

- You get punished for being good at protecting their success

- Asymmetric bargaining power

- You cannot easily withdraw extras without threatening your own revenue

- The client can demand more because “it’s in your interest for us to succeed”

- Your leverage decreases as their dependence increases

This is a structural trap. The more effective you are, the more trapped you become.

Why “just helping” doesn’t create memory #

Just because you help somebody doesn’t mean they’re going to remember that, especially if you don’t enumerate it.

This is the core trap:

- You help because you want them to succeed (and you need them to succeed to get paid)

- They experience your help as continuous support

- Continuous support becomes baseline

- Baseline becomes invisible

- Invisible contributions are not remembered as gifts

You cannot build gratitude from unenumerated help in an outcome-based relationship.

The client is not being malicious. They are responding rationally to the structure. If you keep providing extras without itemizing them, those extras become part of what they think they are paying for.

Example: How this played out in a real consulting relationship #

The setup:

- Consultant brought in on speculation, paid percentage of client sales

- Original scope: maintain existing operations (the “building”)

- Incentive structure: consultant benefits when client succeeds

The drift:

- Client asks for growth work beyond maintenance

- Consultant says yes because they want the client to succeed (and need the revenue)

- Growth work is not separately billed because it is all “percentage of sales”

- Client experiences this as “what the consultant does”

- More requests come

- Consultant absorbs them to protect outcomes

- Baseline keeps expanding

The collision:

- Consultant realizes they are doing construction, chef training, staffing, and marketing

- Consultant tries to return to maintenance-only scope

- Client feels abandoned: “But you’ve always helped with this!”

- Consultant feels exploited: “I’ve been giving you free work!”

Both are right. The ledger was structurally incomplete from the start.

That is Ledger/Visibility Collapse in its purest form. And it was baked into the compensation structure.

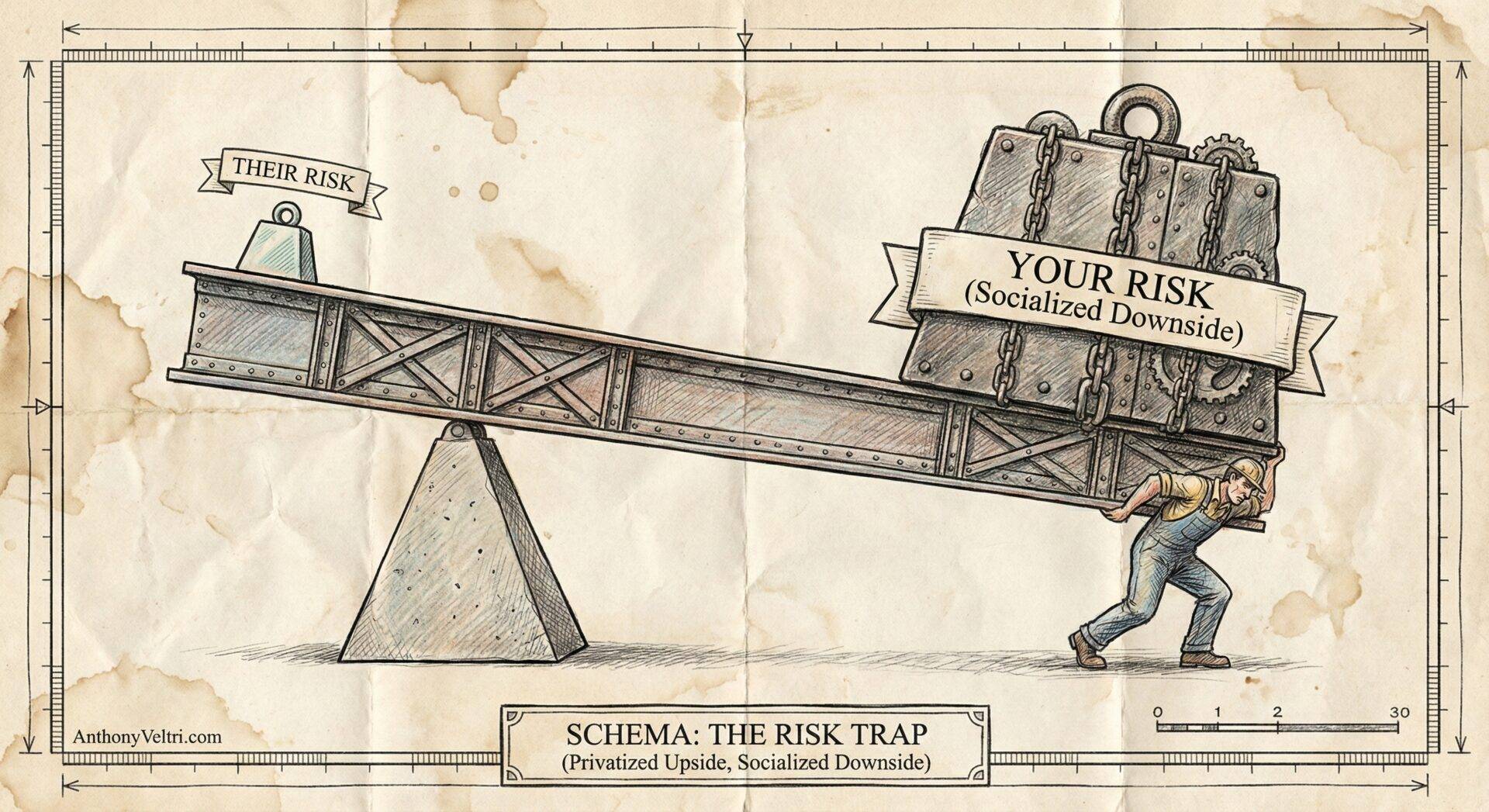

The asymmetric risk trap #

Outcome-based compensation creates scope creep. But there is a second structural problem that makes Ledger/Visibility Collapse genuinely exploitative:

When you absorb all the downside risk but they begrudge you the upside.

The heads-I-win-tails-you-lose dynamic #

Here is how the trap works:

When revenue is high:

- Client sees your percentage payment as a large absolute number

- Client thinks: “You’re being paid too much for what you do”

- Client forgets: the percentage is constant, the risk was yours, the infrastructure was built on speculation

When revenue is low:

- You barely cover your own expenses

- Client expects: continued support at the same level

- Client forgets: you are absorbing the downside without complaint

When client goes on vacation or manages poorly:

- Revenue drops

- You absorb the loss

- This is “just the way it is”

When you built the initial infrastructure:

- All risk was on you

- Client invested nothing upfront

- You built on speculation, hoping for future revenue

This is not a partnership. This is privatized upside, socialized downside.

You carry the risk. They resent the reward.

A small percentage of a large number is a larger number than a small percentage of a small number (obviously). But when that large number arrives, they forget that the percentage stayed constant and the risk was always yours. They just see a big number going to you and think you are being overpaid.

Meanwhile, when the small number arrives (because they went on vacation, or managed poorly, or the market shifted), you absorb it. And that is just “the way it is.”

This is structural exploitation masquerading as partnership.

The Zombie State: The Gap Between Drift and Collapse #

Before a relationship finally collapses, it usually enters the Zombie State. This is the period where the relationship is dead, but it keeps moving because of sunk cost and fear of the void.

You can identify the Zombie State by three specific markers:

1. The Silent Veto (Malicious Compliance) The invisible party stops arguing and starts executing the “Silent Veto.” They don’t quit; they just stop doing the invisible extras.

- They answer the email, but don’t solve the unstated problem.

- They deploy the code, but don’t fix the pre-existing bug.

- They pay the bill, but don’t offer the referral.

Suddenly, things start breaking. The client asks, “Why is this happening?” The answer is, “We are performing exactly to spec.” Malicious compliance is the death rattle of the invisible ledger.

2. The Memory Half-Life In the Zombie State, you realize a painful physics equation: Gratitude has a half-life; Entitlement has a half-life.

“Gratitude has a half-life of about 48 hours. Entitlement has a half-life of forever.” – maybe the author.

- Gratitude decays rapidly (48 hours). If you save the day on Tuesday, it is forgotten by Thursday. You cannot “bank” goodwill in an invisible ledger.

- Entitlement decays never. Once a service is provided twice, it is expected forever.

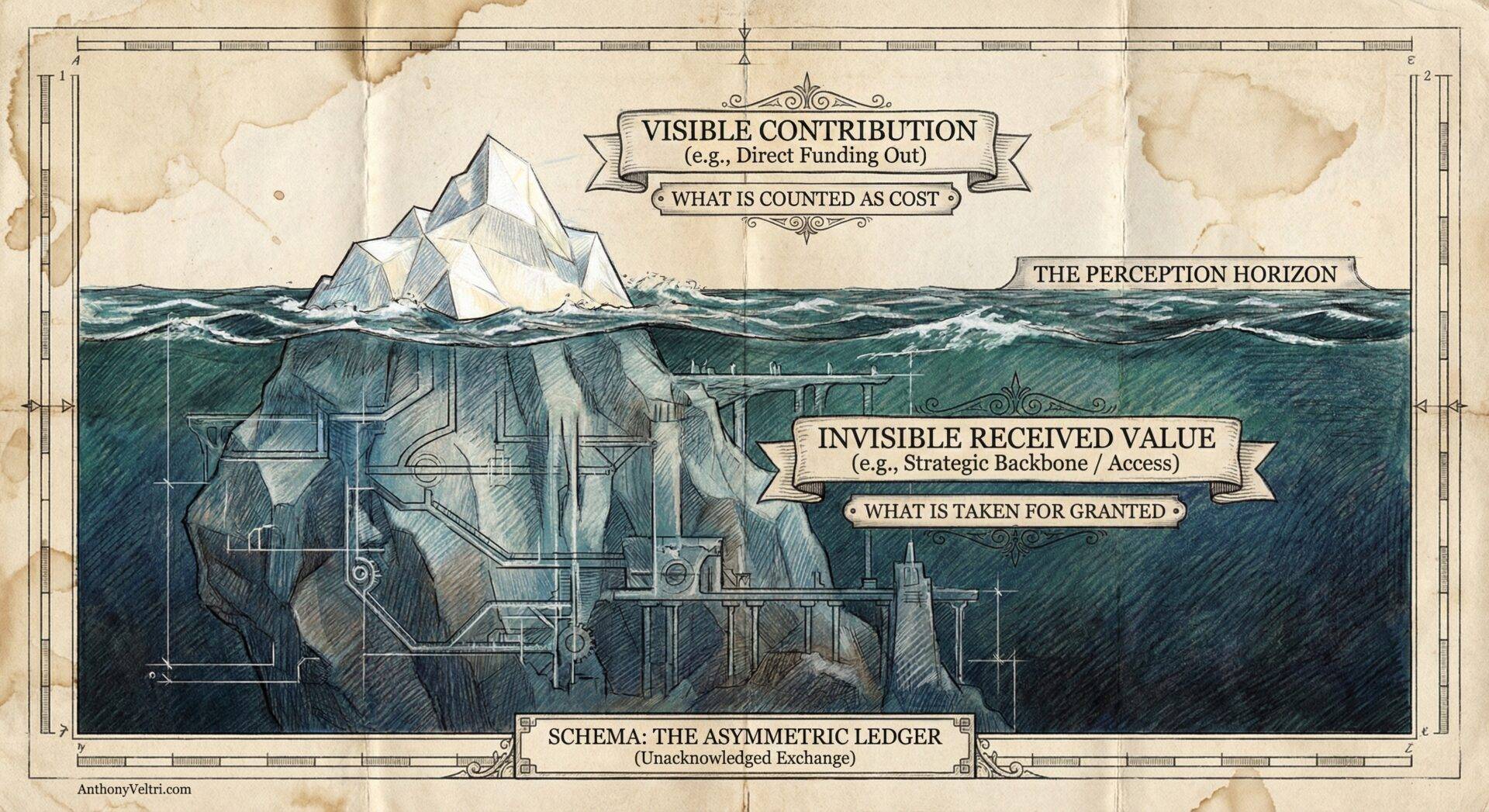

3. The Iceberg Problem The relationship looks stable from the surface, but the physics have changed.

- Above Water (Visible): The Invoice / The Treaty.

- Below Water (Invisible): The Risk / The Access / The Late Nights.

In the Zombie State, the water level (revenue/trust) drops. Suddenly, the ugly, barnacle-encrusted bottom of the iceberg is revealed. The client looks at the massive, messy infrastructure you’ve been managing and says, “What is that ugly thing?”

You say, “That is what was holding you up.”

Why this makes Ledger/Visibility Collapse unfixable #

In a normal Ledger/Visibility Collapse, you can fix it by making contributions visible. Both parties have incomplete ledgers, you publish the full accounting, you rebalance.

But when risk distribution is asymmetric, making the ledger visible does not fix the structure. It reveals the structure is fundamentally exploitative.

Making the ledger visible shows:

- You absorbed all startup risk

- You built infrastructure on speculation

- You carry revenue volatility

- You provide extras to protect outcomes

- They begrudge success but expect support during failure

Publishing that ledger does not create gratitude. It creates defensiveness.

Because what it reveals is: they have been getting a deal that is structurally unfair, and they do not want to acknowledge that.

The European parallel #

This is the same structural problem Europe faces with the US relationship right now.

When US contributions are high (spending, aid, presence):

- US domestic audience sees absolute dollar amounts

- US thinks: “We’re paying too much for what we get”

- US forgets: the structure was built to serve US strategic interests, not as charity

When Europe provides the platform (basing, access, logistics):

- US treats this as background

- US expects: continued access regardless of US behavior

- US forgets: access is conditional, even if the conditions have been generous

When the ledger is published:

- US sees what it provides (spending)

- Europe sees what it provides (access)

- Neither can agree on how to rebalance without risking collapse

Because the fundamental question is: What happens if we try to price this relationship accurately and it turns out one party cannot afford it?

That is the rebalancing dilemma. And it applies to personal relationships, client relationships, and geopolitical alliances equally.

The rebalancing dilemma #

Here is the core problem:

“I don’t know how to rebalance this relationship without risking the possibility of collapsing it entirely.”

This is the honest dilemma. You have three options:

Option 1: Continue as-is

- Accept asymmetric risk distribution

- Accept begrudging during high revenue

- Accept neglect during low revenue

- Burn yourself as fuel

Option 2: Attempt rebalancing

- Make the full ledger visible

- Demand structural changes (upfront payment, tiered pricing, risk sharing)

- Risk: they say no, relationship collapses

Option 3: Accept that collapse is the right answer

- Recognize the structure is fundamentally exploitative

- Recognize they will not voluntarily rebalance

- Walk away cleanly

Most people get stuck choosing between Option 1 and Option 2. They burn themselves out trying Option 1, then attempt Option 2 when they are already resentful and exhausted, which makes the rebalancing conversation confrontational instead of diagnostic.

The key insight is recognizing when Option 3 is actually the right answer from the start.

When collapse is the right answer #

Here is the hard truth:

If the only way to maintain the relationship is to accept structural exploitation, the relationship should collapse.

Or put another way:

“If I’m going to build something on speculation for someone, meaning they haven’t invested anything upfront and all the risk is on me, yet they begrudge me when they have a high month and my percentage is a large number, even though the percentage stays the same, but then they expect you to support them when they are either managing the business poorly or not doing well, maybe that does need to collapse.“

That is not bitterness. That is pattern recognition.

A relationship where:

- You carry all downside risk

- They resent all upside reward

- They expect continued support regardless of their behavior

- Rebalancing attempts are met with defensiveness or threat

That relationship is structurally exploitative. Trying to save it is burning yourself as fuel.

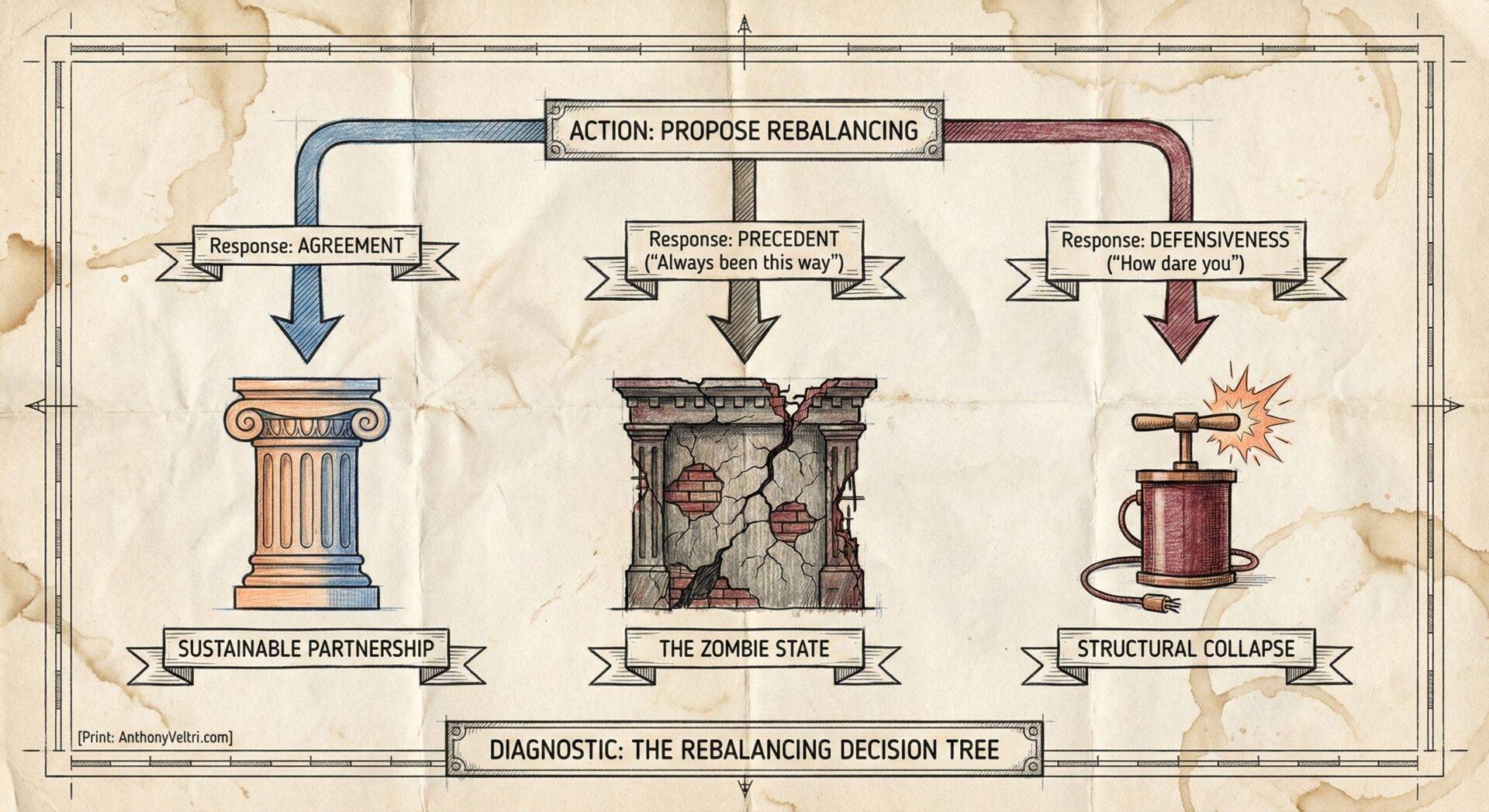

The test for whether rebalancing is possible #

Ask yourself:

If I publish the full ledger and propose structural rebalancing, what are the three possible responses?

Response 1: “You’re right, let’s fix this”

- They acknowledge asymmetric risk

- They propose concrete structural changes

- They follow throliugh

- The relationship is savable

Response 2: “This is how it’s always been”

- They acknowledge the facts but resist change

- They appeal to precedent

- They offer minor concessions but no structural reform

- The relationship is probably not savable

Response 3: “How dare you”

- They get defensive or aggressive

- They threaten withdrawal

- They accuse you of being greedy or disloyal

- The relationship is definitely not savable

If you predict Response 2 or 3, collapse is the right answer.

Because what you are learning is: they know the structure is asymmetric, and they prefer it that way.

At that point, attempting to save the relationship is not noble. It is self-destructive.

Europe’s version of this test #

Europe is facing the same test right now with the US alliance relationship.

If Europe publishes the full alliance ledger and proposes structural rebalancing, what are the possible responses?

Response 1: “You’re right, the relationship is reciprocal, let’s make the full value explicit and maintain it.”

Response 2: “This is how it’s always been, we’ll make minor adjustments but we’re not fundamentally changing the frame.”

Response 3: “How dare you question US generosity, we’ll withdraw and you’ll see what you lose.”

If the US is heading toward Response 3, Europe needs to prepare for collapse as the strategic choice, not as the failure case.

Because trying to maintain a relationship with a party that insists on asymmetric accounting and resents your contributions is not alliance management. It is strategic subjugation.

And sometimes the right answer is: let it collapse.

One more parallel: Afghanistan #

The US spent 20 years in Afghanistan trying to make an unbalanceable relationship work.

The Afghan government:

- Carried no risk (US absorbed it)

- Resented US presence (sovereignty concerns)

- Expected continued support (budget dependence)

- Refused structural reform (corruption, governance)

Every year, the same conversation:

- “We need to rebalance this”

- “Not yet, we’re making progress”

- “Okay, one more year”

The relationship was structurally unbalanceable from the start. Trying to save it was burning soldiers and money as fuel.

The collapse was inevitable. The only question was when.

The same pattern shows up everywhere. Personal relationships, client relationships, institutional partnerships, geopolitical alliances. Once you see it, you cannot unsee it.

You are facing the same pattern recognition: Is this relationship structurally unbalanceable, and am I (we) burning ourself as fuel trying to prevent inevitable collapse?

If yes, collapse is not the failure case. Collapse is the strategic choice.

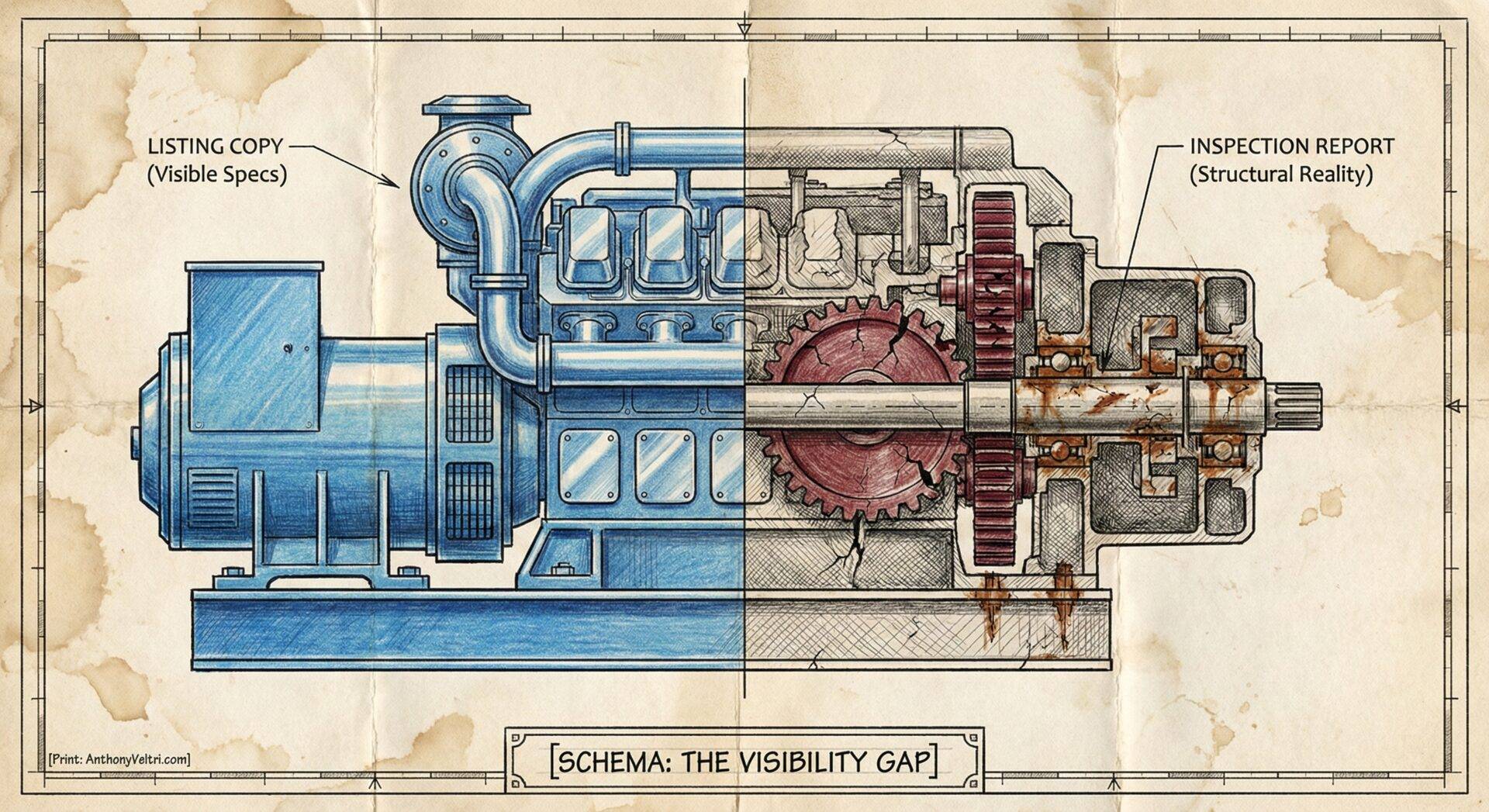

Listing vs inspection (again) #

Ledger/Visibility Collapse is what happens when you mistake listing copy for an inspection report.

Listing: “Defense spending: 2% GDP.”

Inspection: Defense spending, plus basing access, plus logistics throughput, plus intelligence sharing, plus coalition legitimacy, plus regulatory cooperation.

If you only count the listing number, you are defending the wrong artifact.

The visible ledger is listing copy. It is not fraudulent. It is incomplete. It becomes misleading when treated as the whole.

This is the same pattern from Ackshually Gate. When someone says “Ackshually, NATO spending targets say…” they are defending the listing copy while ignoring the inspection report. The narrow definition stops inquiry into the full ledger.

Counter-moves: How to prevent visibility collapse #

You do not fix Ledger/Visibility Collapse by asking for gratitude. You fix it by making the full ledger structurally visible.

Move 1: Publish the inspection report #

Create a simple, repeated narrative that makes all contributions legible:

For geopolitical relationships:

- Here are the key nodes you rely on

- Here is what they enable

- Here is the replacement cost and time if access degrades

For client relationships:

- Here is what was in contracted scope

- Here is what was outside contracted scope

- Here is what outcomes the out-of-scope work created

- Here is what stops if we return to baseline

For personal relationships:

- Here is the visible exchange we both see

- Here is the invisible work that keeps things running

- Here is what changes if the invisible work stops

This is not a guilt trip. This is making the ledger legible before resentment locks in.

The goal is to create a document that both parties can look at and say, “Yes, that is accurate.” If you cannot create that document, you probably have asymmetric risk, not just invisible contributions.

Move 2: Separate extras from baseline structurally #

If you want something to stay visible as “extra,” it must be structurally different from baseline:

- Separate ticketing or billing

- Separate scope documentation

- Separate delivery cadence

- Separate review meetings

If you mix extras into normal delivery, they become invisible by design.

The goal is not to nickel-and-dime. The goal is to prevent historical erasure.

If you are in outcome-based compensation, this becomes critical. You must aggressively enumerate extras or they will disappear.

Create two explicit tiers:

- Tier 1: Baseline operations (what percentage-of-sales covers)

- Tier 2: Growth and optimization (what requires separate agreement)

Make Tier 2 explicitly opt-in with visible tracking.

Keep a running log:

- Date

- Request

- Time invested

- Why it was outside original scope

- Business outcome it created

This is not for billing. This is for making the invisible visible.

Move 3: Price access like access #

If you provide access or enablement (basing rights, platform access, network effects, infrastructure), treat it as a priced asset, not as background.

This does not mean you must charge money. It means you must make the value legible and conditional.

For Europe: Make basing and regulatory access explicitly conditional on reciprocal alliance behavior, not on assumptions.

For you: Make growth work and out-of-scope strategy explicitly conditional on a retainer or add-on, not on spare time.

The goal is not to threaten. The goal is to prevent the contribution from becoming invisible.

Once something is treated as background, it disappears from the ledger. You must keep it visible by making it explicitly conditional.

Move 4: Create periodic ledger reviews #

Schedule explicit reviews where both parties articulate the full exchange:

- What each side provides

- What each side receives

- What is working

- What is becoming invisible

- What needs adjustment

This prevents slow drift into resentment. It creates a structured moment where the full ledger is visible to both parties.

Quarterly is probably the right cadence for most relationships. Annual is too slow (too much drift accumulates). Monthly is too frequent (creates overhead).

The format can be simple:

- 30 minutes

- Both parties bring their version of the ledger

- Compare notes

- Identify discrepancies

- Decide what to adjust

This is not a negotiation. This is a diagnostic conversation. The goal is shared understanding, not winning.

Move 5: Know when collapse is the answer #

Sometimes Ledger/Visibility Collapse is not fixable because the asymmetric structure is the point.

If you:

- Absorb all downside risk

- Get begrudged for upside reward

- Provide invisible extras to protect outcomes

- Face defensiveness when you try to rebalance

The structure is exploitative, not accidental.

Making the ledger visible will not fix this. It will reveal that they know the structure is asymmetric and prefer it that way.

In those cases, collapse is the right answer. Trying to save the relationship is burning yourself as fuel.

The test: If you propose structural rebalancing and predict Response 2 (“this is how it’s always been”) or Response 3 (“how dare you”), the relationship should collapse.

Walk away cleanly. Document the full ledger for yourself, announce your exit, enforce the boundary.

Some relationships are structurally unbalanceable. Recognizing that is not failure. It is pattern recognition.

The way out when collapse is the answer #

If you determine collapse is the right choice, here is how to do it cleanly:

Step 1: Document the full ledger

Not for them. For you.

Write down:

- What you built on speculation

- What risk you carried

- What extras you provided

- What outcomes you created

- What begrudging you received

- What neglect you absorbed

This is your exit artifact. It prevents gaslighting later. When they say “but we always had a good relationship,” or “you’re being unreasonable,” you have the receipts.

You will not send this document to them. But you need it for yourself. To remember that you are not crazy, the structure really was asymmetric, and walking away really is the right answer.

Step 2: Announce the rebalancing conversation

“I need to have a conversation about risk distribution and compensation structure. Here is the current state, here is what needs to change for this to be sustainable.”

Give them one chance to move to Response 1.

Be clear and direct. Do not sugarcoat. Do not apologize. You are not asking for permission. You are announcing a boundary.

Step 3: Accept their actual response

Do not negotiate with Response 2 or 3.

If they resist structural change, that is your answer.

Most people make the mistake of trying to convince them. They argue, they plead, they provide more evidence. That is burning more fuel.

If the response is anything other than “you’re right, let’s fix this,” you have your answer. Move to Step 4.

Step 4: Execute clean withdrawal

“Based on this conversation, I don’t think we can reach a structure that works for both of us. Here is my exit timeline, here is what I will transition, here is what stops.”

No blame. No drama. Just structural incompatibility.

You are not accusing them of being bad people. You are stating that the structure does not work for you and they are unwilling to change it. That is sufficient.

Give them reasonable transition time (30-90 days depending on complexity). Document what you will hand off and what will simply stop. Execute professionally.

Step 5: Enforce the boundary

When they come back with “just this once” or “we need you,” the answer is:

“We already had the rebalancing conversation. The structure didn’t change. My decision stands.”

Do not relitigate. Do not explain again. The boundary is set.

They will test it. Probably multiple times. Hold the line.

This is the hardest part. Because you will feel guilty. You will wonder if you are being unreasonable. You will second-guess yourself.

That is why you created the exit artifact in Step 1. Go read it. Remember the asymmetric risk. Remember the begrudging. Remember that you tried to rebalance and they refused.

You are not being unreasonable. You are protecting yourself from structural exploitation.

When to apply this pattern #

Use Ledger/Visibility Collapse as a diagnostic when you see:

In yourself:

- “They don’t appreciate what I do”

- “I keep giving and get nothing back”

- “They act entitled to my help”

In others:

- “We pay them, what more do they want?”

- “This has always been included”

- “They’re withdrawing support for no reason”

In relationships:

- One party feels exploited

- The other party feels blindsided

- Both parties believe they are being reasonable

- Resentment is building but neither can articulate why

The test: If both parties have incomplete ledgers and both parties feel wronged, you have Ledger/Visibility Collapse.

The distinction from Ackshually Gate #

Ackshually Gate and Ledger/Visibility Collapse are related but distinct:

Ackshually Gate: Weaponizing definitional precision to stop inquiry

- Mechanism: Narrow definition prevents discussion of broader reality

- Example: “That’s not unemployment” stops conversation about household stability

Ledger/Visibility Collapse: Selective accounting makes reciprocal relationships appear one-sided

- Mechanism: Some contributions become invisible while others stay visible

- Example: Defense spending is counted, basing access is not

When they combine: “Ackshually, NATO spending targets say…” stops inquiry into the full alliance ledger.

Both involve collapsed metrics. But one is about conversational derail, the other is about structural invisibility in relationship accounting.

They often appear together because narrow definitions (Ackshually Gate) create incomplete ledgers (Ledger/Visibility Collapse). But you can have one without the other.

One-line definition (portable) #

Ledger/Visibility Collapse is when selective accounting makes reciprocal relationships appear one-sided because some contributions stay visible while others become structurally invisible as baseline.

Companion one-liner (portable) #

The counter-move is not asking for gratitude. The counter-move is making the full ledger structurally visible before resentment locks in, and knowing when collapse is the right answer.

Three diagnostic questions #

Question 1: What am I providing that has become invisible because it is reliable?

Question 2: What are they providing that I have stopped counting because it has become baseline?

Question 3: If we both published our full ledgers, would we discover we are both right about being undervalued?

If the answer to Question 3 is yes, you have Ledger/Visibility Collapse.

Bonus question: If I propose structural rebalancing, do I predict Response 1, 2, or 3?

If you predict Response 2 or 3, collapse is probably the right answer.

Last Updated on January 22, 2026